Step 1: Finances

- Gather your documents

- Obtain pre-approval or proof of

funds - Locate down payment funds

- Budget for any additional costs

By listening to our clients’ needs and goals, we are able to provide unique insight to both buyers and sellers. As we guide clients through purchasing or selling a property, we are able to provide a knowledgeable and experienced opinion of each property. We provide sound and competent advice to buyers and sellers so they can make informed choices about their real estate transactions. Our experience is not only an asset to clients, but also a meaningful advantage for them, providing an added value to their real estate experience.

The initial amount you put to secure the home for our offer. This ranges from 2% to 3% and is reduced from your final down payment. This can be done in one deposit or split into two payments

Home inspections are important when buying a home. We want to find out everything we can that could be wrong with the home. A general home inspection is a must, but you can also select the termite / pest inspection, radon inspection, water inspection (if well water), septic inspection (if on-site septic), stucco inspection, and lead paint inspection.

All homes that have a mortgage will require an appraisal to ensure that the home is valued correctly. An appraisal is done strictly for the lender and costs between $400 - $575. This will be paid upfront but will be reduced from your total closing costs.

This is not due in full until closing day! Typically ranging from 3.5% (with an FHA loan) to 20%,and everywhere in between!

Closing costs are the fees that are needed to close and get keys for your new home – such as lender fees, transfer tax,escrow (including your taxes), reimbursements, and homeowners insurance. Closing costs typically range from 3%-5% of the purchase price of the home.

***It Is Also Important to Elect Property & Flood Insurance to Make Sure that There Were No Major Claims on The Property that Were Not Disclosed!

*Costs May Vary Depending on The Inspection Company Used

The very first step of the home buying process is to get a pre-approval letter from a lender stating how much you are qualified for.

A pre-approval is only valid for 30-90 days, so while you can start talking to lenders, you’ll want to wait on getting that pre-approval letter when you’re ready to buy.

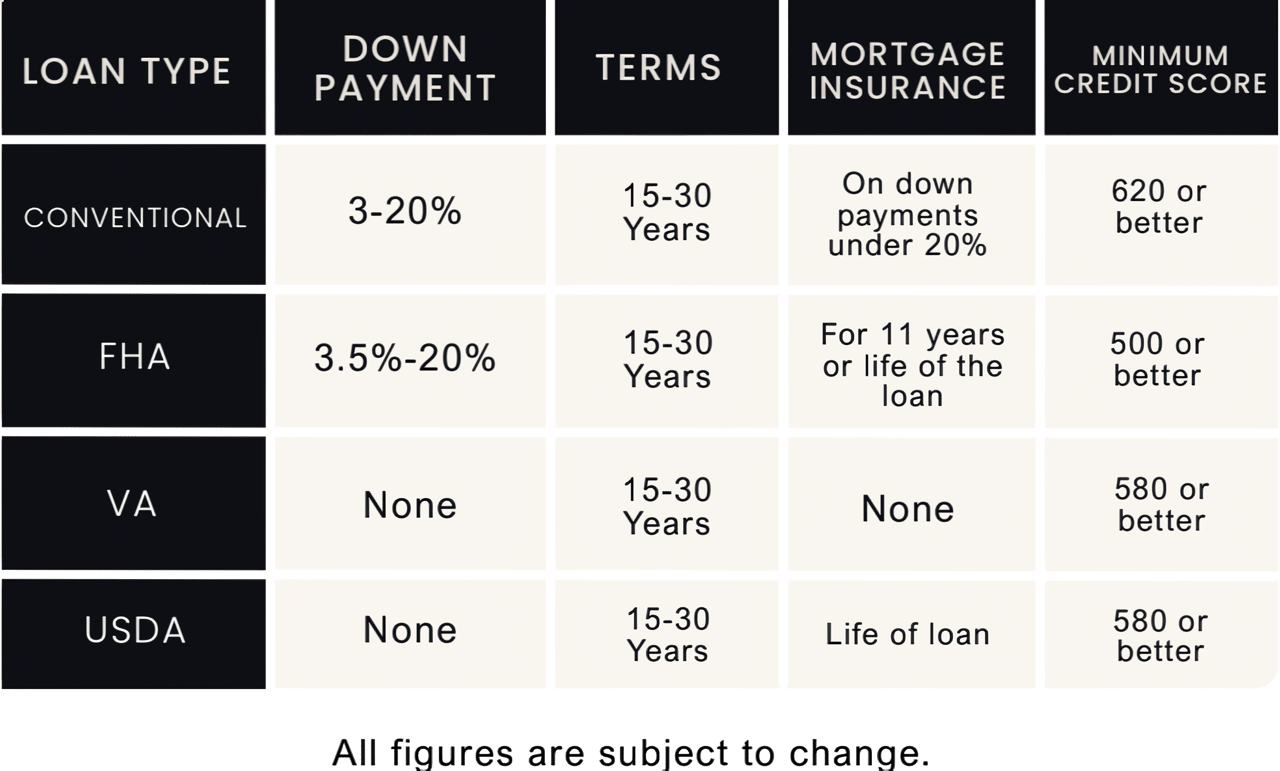

Which type of loan is right for you?

CONVENTIONAL LOAN

The most common type of home loan, which is offered through private lenders.

FHA LOAN

Loans designed for those with high debt-to-income ratios and low credit scores, and most commonly issued to first-time homebuyers. Offered by FHA-approved lenders only and backed by the Federal Housing Administration.

VA LOAN

Loans designated for veterans, spouses, and reservists, offered through private lenders and

guaranteed by the U.S. Department of Veteran Affairs.

USDA LOAN

Loans for homebuyers in designated rural areas, backed by the U.S. Department of Agriculture.

There are certain “Do’s and Don’ts” which may affect the outcome of your loan request. These remain in effect before, during, and after loan approval up until the time of settlement when your loan is funded and recorded. Many times, credit, income, and assets are verified the hour before you have signed your final loan documents.

Once you’ve got your finances in order, the fun of looking for the perfect home begins!

I will set you up on an automatic search through the Multiple Listing Service (MLS), which is the database that Realtors use to list and search for homes. The moment a home that fits your search criteria is listed for sale, it will be sent directly to your email inbox. If we ever need to adjust the search criteria, just let me know and I can make any changes you need.

During the inspection period, the buyer has the right to hire a professional to inspect the condition of the home. The inspection will uncover any issues in the home that would have otherwise been unknown

The standard home inspector’s report will cover the condition of the home’s heating system; central air conditioning system; interior plumbing and electrical systems the roof, attic, and visible insulation; walls, ceilings, floors, windows, and doors; the foundation, but I recommend you attend the inspection.

RADON INSPECTION- Radon gas is the 2 leading cause of lung cancer in the US. It is a naturally occurring gas that is colorless and odorless

TERMITE INSPECTION - Ask your lender if your loan requires any certain inspections such as a Wood Destroying Organism (WDO) inspection

LEAD-BASED PAINT INSPECTION - If the home was built prior to 1978, a lead-based paint inspection is recommended.

WELL WATER / SEPTIC INSPECTION - If the home has a septic system or well water to make sure the water is not contaminated and the septic system is working properly

HOMEOWNERS

The standard homeowners insurance covers financial protection against loss due to disasters, theft, and accidents.

HAZARD

Hazard insurance protects against damage caused by fires, severe storms, hail/sleet, or other natural events.

FLOOD

Protects against damage caused by a flood.

WINDSTORM

Protects against damage caused by events such as tornadoes, hurricanes, or gales

TITLE: The title company will conduct a title search to ensure the property is legitimate and find if there are any outstanding mortgages, liens, judgements, restrictions, easements, leases, unpaid taxes, or any other restrictions that would impact your ownership associated with the Property. Once the title is found to be “clear”, the title may rise over ownership of the property. This is required when obtaining a mortgage and is highly recommended even if you are paying cash. This will also be a part of your closing costs, and the fees are state-regulated, which means every title company will charge the same amount for title insurance, making it easier for you because you don’t need to “shop around”!

“CLEAR TO CLOSE” IS EXCELLENT NEWS! - It means the mortgage underwriter has officially approved all documentation required to fund the loan. All that remains is the actual closing process.

FINAL WALKTHROUGH - We will perform a final walk-through the day of settlement to confirm that the seller made the repairs that were agreed upon and to make sure no issues have come up while under contract.

The listing agent has a fiduciary duty to the seller by signing a contact with them first, you as a buyer are a second interest. If you went to court, would you use the other person’s attorney? Of course not, you want an experienced agent working for you to get the best price and terms that is best suited for YOU, not all one-sided for the seller!

Work with an agent to negotiate better terms or upgrades in your new home that the builders often do not tell buyers because they have the builder’s best interest and profit in mind – not yours. Your agent also recommend which upgrades to do now with the builder, and what would make more sense to do after you move in. Not to mention, if anything were to go wrong during the process, you would definitely want someone representing YOU and your best interest, which is not the sales rep, as they work for the builder.

Though many foreclosure homes are perceived as an excellent investment due to lower than average pricing, there are a few stipulations to consider. Many foreclosed homes are in a rough condition due to previous owners being forced out of their homes. With this in mind, the properties are rarely left in “move-in” condition and are always being sold as- s with an extremely rare chance to have the home fixed prior to the purchase. While typical escrows last 30-45 days, due to the complicated nature of the loans, these escrows take a minimum of 90-120 days to close and receive keys.

59 N Main St Mullica Hill, NJ 08062

59 N Main St Mullica Hill, NJ 08062